Due to Asia´s advanced position (with China at the forefront) in strategic industries such as batteries, there are two regions that are making the most progress in order not to miss this train: Europe and North America. Below, we take a closer look and update you on the main advances made by both regions in this regard.

EUROPE AND ITS ´MATCHING AIDS´: RESPONDING TO THE GLOBAL CHALLENGE

In recent months, and as we have been seeing in different posts on our social networks, Europe has taken significant steps in restructuring its economic policies, with a special focus on gaining competitiveness in terms of renewable energies and green technology.

The articulation of this strategy is taking place through different formulas, including the already analyzed "EU Net-Zero Industry Act" or the well-known "matching aids". The latter (already in existence before this "fever" for green investments) consist of financial aid offered by governments or supranational entities such as the European Union (EU) to support and encourage investment in specific projects, especially in strategic sectors such as technology, research and development, and renewable energies.

Their name derives from the requirement that the beneficiary of the grant (which may be a company, research institution, or other entity) also contribute an amount of funds, so that the government support "matches" or "complements" the private or internal investment of the entity.

A clear example of this support is the €900 million capital injection that Germany has recently granted to Northvolt. This investment has been earmarked to secure the construction of the Swedish manufacturer´s new battery gigafactory in Germany, which not only strengthens Europe´s technological capacity, but also represents an effort to maintain investment and talent within the European bloc.

It is worth noting that this was the first European project financed through this formula, but it is already expected that more European countries will follow this trend, especially in response to the challenges posed by foreign policies such as those of North America (with the USA, and to a lesser extent Canada, leading the way).

U.S.: THE IMPACT OF THE INFLATION REDUCTION ACT (IRA)

Almost a year and a half after the implementation of the IRA, it can be said that the balance sheet for the US government is very positive, thanks to its impact and carry-over effect. As we have already analyzed, thanks to this regulation (which encourages green investments on US soil thanks to a combination of tax incentives, grants and loan guarantees), it has begun to redefine the investment landscape in the US, attracting funds that originally could have been directed to other territories.

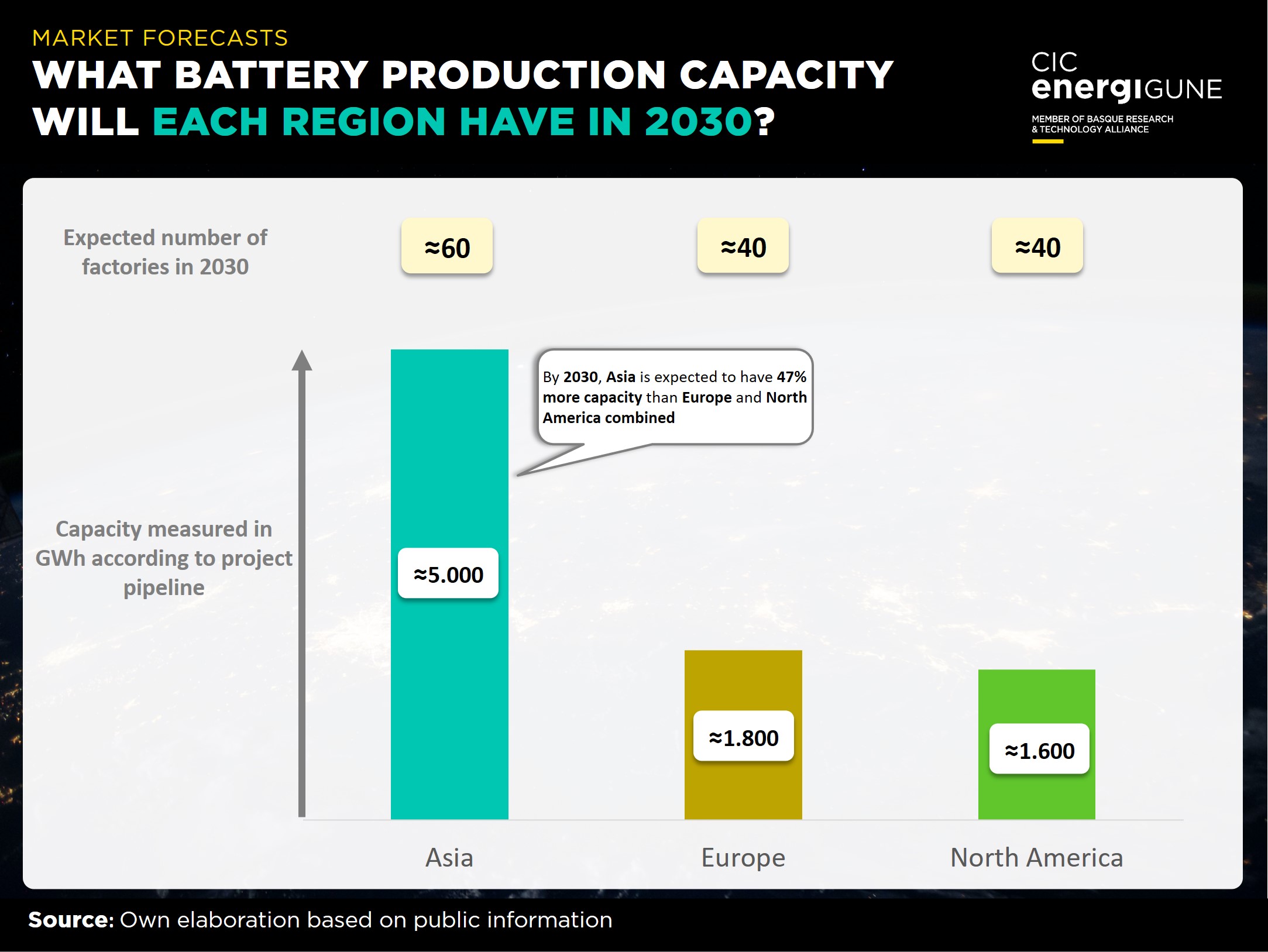

The implementation of the Inflation Reduction Act (IRA) in the US has been a crucial catalyst for the growth of gigafactory projects in North America, significantly boosting its battery industry. By the close of 2023, North America, with the U.S. leading the way, has managed to match Europe in terms of number of gigafactory projects, with both regions counting around 40 ongoing and planned initiatives. This equality in the number of projects is a clear indication of North America´s rapid progress in this field, largely enabled by IRA incentives and policies.

In terms of manufacturing capacity, North America is expected to reach 1,600 GWh according to its current pipeline of projects, while Europe is projected at around 1,800 GWh. All these figures will surely continue to increase considering the pace of investments in recent months.

Despite this remarkable growth, both regions still lag behind Asia, especially China, which dominates the market with almost 60 projects in its portfolio. Many of these gigafactories in Asia are already operational, with ambitious expansion plans. In particular, China stands out with more than 25 operational or planned plants, representing a cumulative capacity of approximately 2,500 GWh, contributing significantly to Asia reaching 5,000 GWh in battery manufacturing capacity.