In our analysis carried out in April last year, we noted how North America (with the USA at the forefront) was seeking to take positions within the "battle" that is expected to take place in the future of the gigafactories industry between different regions of the world (especially concerning Asia and Europe).

After almost a year of announcements and advances, it can be said that the subcontinent has not wasted any time accelerating its plans for the development of large gigafactory projects, sponsored mainly by the interests and investments of the leading OEMs in the region.

A clear example of this is GM and Ford, two of the members of the U.S. "big three" vehicle manufacturers, together with Chrysler. They have been the main drivers of the market in recent months, thanks to their intentions to develop macro-projects on U.S. soil that will enable them to speed up the electrification of their fleets.

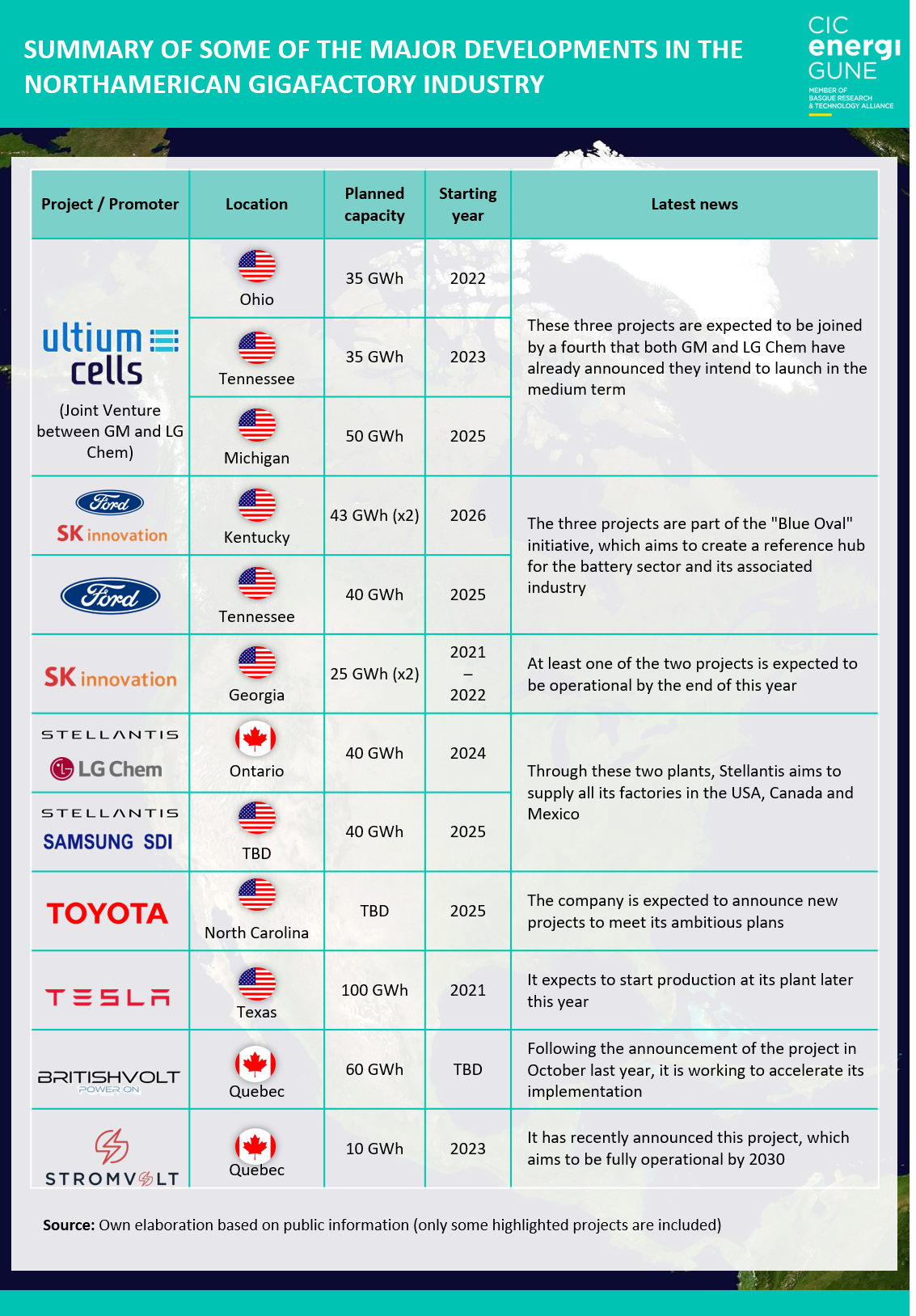

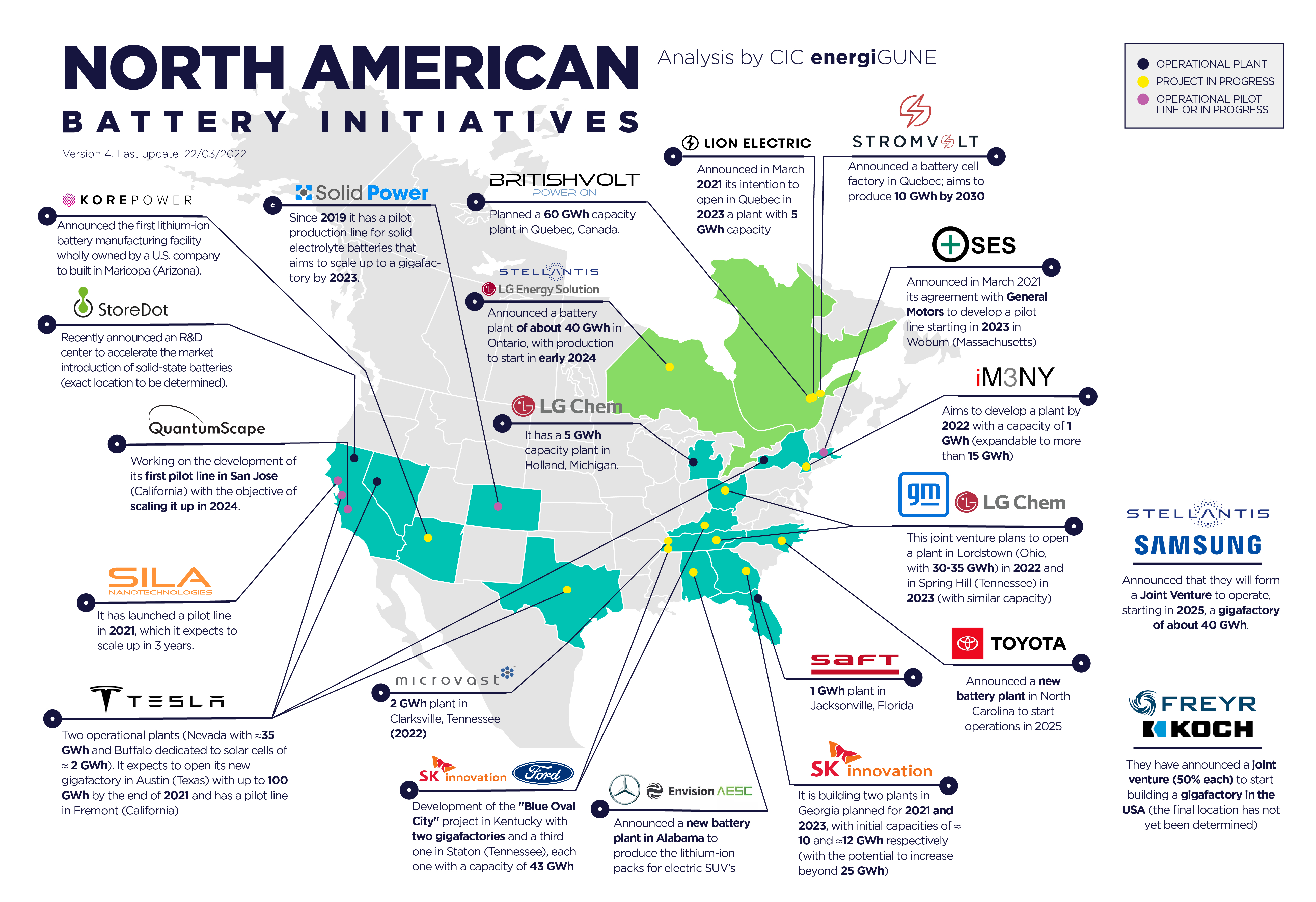

GM is currently the company with the most extensive portfolio of planned projects, with plans to develop four factories thanks to its collaboration with the Korean company LG Energy Solutions. Both companies have established a joint venture called "Ultium Cell" with which they aim to lead the sector and which is responsible for the development of these plants.

Two of them are expected to go into production in the short term; specifically, the Lordstown plant in Ohio - scheduled for August 2022 with a capacity of 35 GWh - and the Spring Hill plant in Tennessee - planned for the end of 2023 with a capacity of 35 GWh. In addition to these, the plant planned for Lansing, Michigan (the heart of the American automotive industry), which is expected to have a capacity of 50 GWh, will join them in 2025. Additionally, both companies have announced that they intend to develop a fourth project, although no further information on capacity or location has yet been provided.

Against this backdrop, Ford is not far behind, thanks to its collaboration with the Korean company SK Innovation. In this case, three major projects are expected to be launched between 2025 and 2026, as part of the initiative known as "Blue Oval City". This large-scale project, planned by the two companies, will create a facility of more than 15 million square meters in the state of Kentucky around electric mobility, which will include, among others, two gigafactories with a production capacity of 43 GWh each, starting in 2026.

Moreover, this initiative includes a third project in the state of Tennessee, which is also expected to have a capacity of around 40 GWh once the initiative is scaled up after its opening in 2025. SK Innovation is also working on its own on two other initiatives, both located in the state of Georgia and expected to be operational between this and next year with expected capacities of up to 25 GWh.

The arrival of other major manufacturers

Beyond these major plans led by U.S. companies, other major manufacturers have also recently announced their intention to participate in the deployment of the sector on North American soil.

This is the case of the Stellantis group (which includes the third US giant, Chrysler), which has announced the development of two projects with estimated opening dates between 2024 and 2025, although still without a definitive location. What is unique in its case is that each of them will be carried out in collaboration with a different technologist: on the one hand, with LG Energy Solution - with a planned capacity of up to 40 GWh - and on the other with Samsung SDI, with whom it has created a joint venture for the implementation of this project, which also aims to reach 40 GWh.

Another of the sector´s leaders, Toyota, has also announced its expansion plans in the US within the gigafactories industry. The Japanese company, one of the most ambitious in terms of fleet electrification, announced last December its first project in the US, where it will develop a plant in the state of North Carolina with the aim of starting operations in 2025. The final capacity of the plant has not yet been disclosed.

Two German giants have also set their sights on U.S. territory, taking their first steps to develop their battery production capacity.

This is the case, for example, of Mercedes-Benz, which will start working with its supplier Envision AESC to develop facilities near its plant in Tuscaloosa (Alabama), with the aim of starting to supply one of its main car production plants and laying the foundations for a subsequent scale-up that will result in its first gigafactory in the USA.

Volkswagen is working similarly at the moment, having launched last November in Chattanooga (Tennessee) a "pilot line" to start testing on North American soil its battery manufacturing capabilities for a later scale-up.

This is joined by other projects with European capital, such as FREYR, a Norwegian company specialized in battery production, which, with the collaboration of Koch Strategic Platforms and the technology of 24M Technologies, aspires to develop a 50 GWh plant in the USA. The final location of the plant is expected to be announced later this year.

These projects, together with other significant initiatives that have been underway for months, such as Tesla´s project in Austin (with a planned capacity of 100 GWh), are making the USA a hub of reference and a player to be taken into account in the future of a key industry for the world.